Inclusion means Exclusion

Mr. Abhishek Mishra,

Article Written by: Mr. Abhishek Mishra, AIBS Student

Date: 10-Jan-2012

What saved India from the devastating outcomes of the global meltdown? The reason is somewhat similar to what happened in China. Yes, the Domestic Demand of both the countries was so strong that it saved them from the contagious effect of economic slowdown. But will India again be able to regain if another blow comes from the International sentiments? The pictures become vague if we take into consideration the current circumstances which are spoiling the image and efficiency of India. E.g. the uncontrollable inflation rate, slump in manufacturing sector, changing decisions on FDI in multi retail, continuous fall of rupee, Corruption, these all have become a prudent challenge for the Indian Economy and obviously for Indian Legislatives. There are ample amount of areas where an immediate change is very much important to tackle the situation. We’ll talk about Financial Inclusion- one of the important areas that can bring marvels for India.

Date: 10-Jan-2012

What saved India from the devastating outcomes of the global meltdown? The reason is somewhat similar to what happened in China. Yes, the Domestic Demand of both the countries was so strong that it saved them from the contagious effect of economic slowdown. But will India again be able to regain if another blow comes from the International sentiments? The pictures become vague if we take into consideration the current circumstances which are spoiling the image and efficiency of India. E.g. the uncontrollable inflation rate, slump in manufacturing sector, changing decisions on FDI in multi retail, continuous fall of rupee, Corruption, these all have become a prudent challenge for the Indian Economy and obviously for Indian Legislatives. There are ample amount of areas where an immediate change is very much important to tackle the situation. We’ll talk about Financial Inclusion- one of the important areas that can bring marvels for India.

|

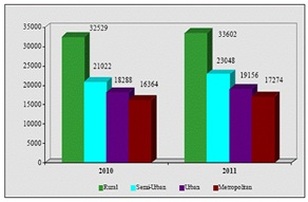

Let take a walk in to the background of Indian Financial System. It is estimated that about 40% of Indians lack access even to the simplest kind of formal financial services, about 500,000 villages are yet to be provided with banking services out of the total 600000 villages present in India. The distribution of branches as shown by the graph depicts the actual picture of Indian Financial System and its reach to population. The graph shows Population Group-Wise Distribution of Number of Officesof Commercial Banks - 2010 And 2011. As a result low-income Indian households in the informal or subsistence economy often have to borrow from friends, family or usurious moneylenders. They have little awareness and practically no access to insurance and financial products that could protect their financial resources in unexpected circumstances such as illness, property damage or death of the primary breadwinner.

|

|

Now can we imagine of an inclusive and prominent growth f India without including the Great Souls of India as mentioned by Mahatma Gandhi? The answer is no doubt “No”. So what can be the solution for this, we’ll discuss it here after.

The Catalyst

Financial inclusion is the process of ensuring access to appropriate financial products and services needed by vulnerable groups such as weaker sections and low-income groups at an affordable cost in a fair and transparent manner by mainstream institutional players. Financial inclusion has become one of the most critical aspects in the context of inclusive growth and development. It leads to more comprehensive growth where in each and every individual of the country would be able to use the financial resources to cater his or her needs to make optimal utilization of resources that will actually reap the fruits of nation’s progress. In India, the term financial inclusion first featured in 2005, when RBI, in its annual policy statement of 2005-06, while recognizing the concerns in regard to the banking practices that tend to exclude rather than attract vast sections of the population, urged banks to review their existing practices to align them with the objective of financial inclusion. It encouraged expansion of bank branches, especially in rural areas, resulting in multifold increase in branch network from around 8,000 in 1969 to more than 89,000 today.

The outcomes are really revolutionary. It will boost the commercial activities right from the grass root levels. Financial regulation will be far more effective and efficient. It will reduce the rate of migration that is happening from rural to urban sectors. India will move on its domestic demand and the magnitude of dependency on global factors will drastically reduce leading to a safeguard for Indian economy form any external shocks. Financial inclusion will increase the money flow leading to more production and reduced food inflation. Education and literacy rate will improve that will bring a social up gradation for rural societies and the counting is still going.

Bottlenecks of the Road

The major barriers to serve the poor, apart from socioeconomic factors such as lack of regular income, poverty, illiteracy, etc., are the lack of reach, higher cost of transactions and time taken in providing those services. Products designed by the banks are not tailored to suit the needs of low-income families. The existing business models do not pass the test of scalability, convenience, reliability, flexibility and continuity. Expectations of poor people from the financial system is security and safety of deposits, low transaction costs, convenient operating time, minimum paper work, frequent deposits, and quick and easy access to credit and other products, including remittances suitable to their income and consumption.

The unorganized structure of villages also create amount of hindrances for the effective execution of Financial Inclusion. Now there is always a profitability factor involved for the banks while thinking for expansion and until and unless it seems feasible for banks to expand without incurring losses, the project will be hanging in between.

The Catalyst

Financial inclusion is the process of ensuring access to appropriate financial products and services needed by vulnerable groups such as weaker sections and low-income groups at an affordable cost in a fair and transparent manner by mainstream institutional players. Financial inclusion has become one of the most critical aspects in the context of inclusive growth and development. It leads to more comprehensive growth where in each and every individual of the country would be able to use the financial resources to cater his or her needs to make optimal utilization of resources that will actually reap the fruits of nation’s progress. In India, the term financial inclusion first featured in 2005, when RBI, in its annual policy statement of 2005-06, while recognizing the concerns in regard to the banking practices that tend to exclude rather than attract vast sections of the population, urged banks to review their existing practices to align them with the objective of financial inclusion. It encouraged expansion of bank branches, especially in rural areas, resulting in multifold increase in branch network from around 8,000 in 1969 to more than 89,000 today.

The outcomes are really revolutionary. It will boost the commercial activities right from the grass root levels. Financial regulation will be far more effective and efficient. It will reduce the rate of migration that is happening from rural to urban sectors. India will move on its domestic demand and the magnitude of dependency on global factors will drastically reduce leading to a safeguard for Indian economy form any external shocks. Financial inclusion will increase the money flow leading to more production and reduced food inflation. Education and literacy rate will improve that will bring a social up gradation for rural societies and the counting is still going.

Bottlenecks of the Road

The major barriers to serve the poor, apart from socioeconomic factors such as lack of regular income, poverty, illiteracy, etc., are the lack of reach, higher cost of transactions and time taken in providing those services. Products designed by the banks are not tailored to suit the needs of low-income families. The existing business models do not pass the test of scalability, convenience, reliability, flexibility and continuity. Expectations of poor people from the financial system is security and safety of deposits, low transaction costs, convenient operating time, minimum paper work, frequent deposits, and quick and easy access to credit and other products, including remittances suitable to their income and consumption.

The unorganized structure of villages also create amount of hindrances for the effective execution of Financial Inclusion. Now there is always a profitability factor involved for the banks while thinking for expansion and until and unless it seems feasible for banks to expand without incurring losses, the project will be hanging in between.

Remedies

But there are a number of ways through which inclusion of all the sphere of societies can happen and which can be discussed as follows:-

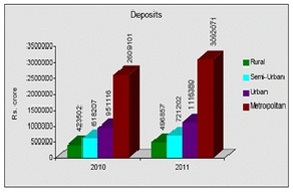

1. Banks should come up with comprehensive plans to cover the areas which are still out of the financial reach by setting up new branches in rural and sub urban areas. It will help banks to increase the amount of deposits that it gets from rural and sub urban areas. The chart beside clears the picture of total deposits that banks get from Rural, Sub urban, Urban and Metropolitan areas.

2. Since the disposable income and saving of a rural individual is very less, banks should make provision of No- Frills accounts where people can open and maintain their banks accounts with a very small amount also.

3.The cumbersome procedure of opening a bank account and the documents required by the bank is really a complex task and it leads to perplexing the rural people. Hence the process should be made a bit easy and customized.

4. The banks can also come up with customized products and services to promote the banking services. Since there is remarkable difference in the way transactions happen in Urban and Rural areas. This will help in providing customers with quality banking services at their doorstep and at the same time generating business opportunities for the banks. Easy to access credit is one of such products that banks have come up to lure the rural and sub urban population.

1. Banks should come up with comprehensive plans to cover the areas which are still out of the financial reach by setting up new branches in rural and sub urban areas. It will help banks to increase the amount of deposits that it gets from rural and sub urban areas. The chart beside clears the picture of total deposits that banks get from Rural, Sub urban, Urban and Metropolitan areas.

2. Since the disposable income and saving of a rural individual is very less, banks should make provision of No- Frills accounts where people can open and maintain their banks accounts with a very small amount also.

3.The cumbersome procedure of opening a bank account and the documents required by the bank is really a complex task and it leads to perplexing the rural people. Hence the process should be made a bit easy and customized.

4. The banks can also come up with customized products and services to promote the banking services. Since there is remarkable difference in the way transactions happen in Urban and Rural areas. This will help in providing customers with quality banking services at their doorstep and at the same time generating business opportunities for the banks. Easy to access credit is one of such products that banks have come up to lure the rural and sub urban population.

|

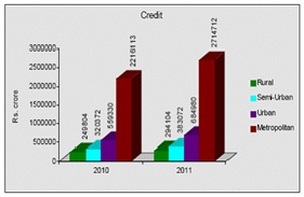

5. Engagement of business correspondents is also a feasible option for banks where banks can contact agents and intermediaries to provide financial services to common public. The BC model allows banks to provide doorstep delivery of services, especially cash in-cash out transactions, thus addressing the last-mile problem, hence leading to substantial increase in the total amount of credit facilities provided by Indian Banks to Rural people. The graph shows the segregation of credit facilities being provided

6. Greater use of technology is an another option that the banks can exercise. Services like mobile banking and web based banking have the possibility of increasing the reach of financial services in all over the nation |

|

7. Along with the above measures banks should also run an awareness campaign to educate the target customers, education level of the population demands this measure to be taken.

8. Mindset, cultural and attitudinal changes at grass roots and cutting-edge technology levels of branches of banks are needed to impart organizational resilience and flexibility. Banks should institute systems of reward and recognition for personnel initiating, ideating, innovating and successfully executing new products and services in the rural areas.

Conclusion

The dream of seeing India growing inclusively will always be incomplete if we cannot include the grass root level factors into the whole picture. Until and unless we include and help in the growth of our spinal entrepreneurs, we will not be able achieve an inclusive growth. History of other countries shows that economic growth follows financial inclusion. The growth comes after the business opportunities being provided by the financial measures and thus increases the national and gross domestic product. And hence it’s the road that India need to travel to become a global player. Financial access and increasing GDP with an increased rate of manufacturing output will definitely attract foreign money onto the economy which will lead to further growth and development of the whole country. Financial Inclusion is an act of Empowerment that will allow people to participate more in the economic and social processes of India. Therefore we can say that Inclusion of grass root level economic activities in to the financial system leads to the exclusion of much such vulnerability that can impact the growth and development of Indian Economy.

References:-

1. Statistics are supported by RBI database.

8. Mindset, cultural and attitudinal changes at grass roots and cutting-edge technology levels of branches of banks are needed to impart organizational resilience and flexibility. Banks should institute systems of reward and recognition for personnel initiating, ideating, innovating and successfully executing new products and services in the rural areas.

Conclusion

The dream of seeing India growing inclusively will always be incomplete if we cannot include the grass root level factors into the whole picture. Until and unless we include and help in the growth of our spinal entrepreneurs, we will not be able achieve an inclusive growth. History of other countries shows that economic growth follows financial inclusion. The growth comes after the business opportunities being provided by the financial measures and thus increases the national and gross domestic product. And hence it’s the road that India need to travel to become a global player. Financial access and increasing GDP with an increased rate of manufacturing output will definitely attract foreign money onto the economy which will lead to further growth and development of the whole country. Financial Inclusion is an act of Empowerment that will allow people to participate more in the economic and social processes of India. Therefore we can say that Inclusion of grass root level economic activities in to the financial system leads to the exclusion of much such vulnerability that can impact the growth and development of Indian Economy.

References:-

1. Statistics are supported by RBI database.